The Future Of The House Of Mouse

Disney's future hinges on a giant pivot, one that its newest CEO might be uniquely positioned to engineer

In March Disney’s board unanimously elected Josh D’Amaro as its next CEO. The 28-year company veteran previously oversaw theme parks, cruises, resorts, consumer products, and video games. Under his leadership, the Experiences division has become Disney’s profit engine, accounting for 55% to 70% of the company’s total profits since fiscal 2022.

The selection of Josh D’Amaro over Dana Walden, who runs Disney’s film, television, and streaming businesses, is being read by most analysts as a straightforward endorsement of Disney’s most profitable division. Parks are booming, content is struggling, so Disney picked the parks guy.

The story, however, is much bigger than that, but not in the manner Disney probably intends.

D’Amaro’s appointment comes at a time when Disney is dealing with several existential and structural problems that it hasn’t solved and may not even fully recognize. But it also puts someone in the CEO chair who just so happens to sit on top of the exact assets that could solve them, if he’s willing to think far beyond what the board likely hired him to do.

Problem #1: The Content Funnel Is Narrowing Into a Chokepoint

The implicit logic of choosing a parks-and-experiences CEO over a content CEO is that Disney views its content arm as a funnel. Disney, over the last three decades or so, has comfortably settled into a dynamic. You make films and shows to generate IP, characters, worlds, and stories that can then be extended across parks, cruises, games, merchandise, and every other experience touchpoint. The content is fuel. The experiences are the product. Iger had essentially said as much on the most recent earnings call: the strategy is big movies that drive consumer products, drive theme park attractions, drive rides.

The logic is clean, and it’s not necessarily wrong. A single franchise like Frozen, beyond its theatrical run, can generate billions across merchandise, themed lands at every global park, cruise ship entertainment, a walking robot, and eventually a persistent digital world. The return on that one piece of IP dwarfs the return on a well-reviewed Hulu original that lives and dies on the streaming platform.

But this logic has a dangerous corollary, and it may already be playing out. If content exists primarily to feed the experience machine, the incentives are to consolidate investment around the fewer and bigger bets that spawn franchises and tentpoles that can power every other business line. Why spread resources across 20-30 projects a year when what you really need are five massive swings that each generate a multi-billion-dollar IP ecosystem?

There are signs this consolidation is accelerating. Iger said at the closed-door Allen & Co Sun Valley conference that general entertainment is “not Disney’s forte” and that linear TV may be “noncore.” He later walked this back, but the underlying logic and the fundamental facts have not changed. A large percentage of their media business is non-essential to the core business.

Rich Greenfield of Lightshed Media predicted that within 18 months, Disney would move toward a corporate separation, spinning off ESPN, ABC, and its linear TV assets, similar to the now-scrapped split of Warner Bros. Discovery. That prediction comes on the heels of Disney+ increasingly being repositioned as an outlet for movies rather than a TV content platform. Hulu is being folded into Disney+ later this year. That move has raised increasingly uncomfortable questions about the tens of billions spent to buy out Comcast’s stake in the platform.

If this trajectory continues, Disney’s content apparatus narrows substantially. And that creates massive single points of failure. In a diversified content model spanning TV shows, streaming originals, and theatrical releases across multiple studios, the company takes about 20-30 shots on goal per year. Some miss, but the portfolio absorbs the cost of those failures with the success of the hits.

If Disney plans to narrow that to a handful of tentpole films and a streaming platform that exists to extend their shelf life, then each one of those shots carries enormous weight. If two or three underperform in a given year, you haven’t just had a bad year at the box office; you’ve starved the entire experience ecosystem of fresh IP to build on. Moreover, it creates a serious quarter to quarter volatility risk for the company and its stock price.

2025 was a strong theatrical year, with Lilo & Stitch and Zootopia 2 both crossing $1 billion, but that followed several years of underperformance that had shaken investor confidence. It is also worth noting that both those movies are remakes or sequels to existing IP rather than new IP.

With this now-completed succession, there is a deeper issue here too, and it’s one that Puck News’ Matt Belloni put sharply: D’Amaro has spent his entire career exploiting existing franchises at the parks, not creating new ones. Disney has excelled at milking Marvel, Star Wars, Pixar, and its animated classics, but it hasn’t created a major new franchise in years.

Disney+ has produced hits (Only Murders in the Building, Paradise, Percy Jackson), but nothing that’s become a platform-defining cultural phenomenon on the level of Stranger Things or Yellowstone. Their biggest streaming hit, Bluey, is content Disney doesn’t even own. If the content arm is planning to narrow and the person running the company has no track record in IP creation, where will the next Frozen-scale franchises come from?

Problem #2: The Experiences Bet Assumes People Can Afford Experiences

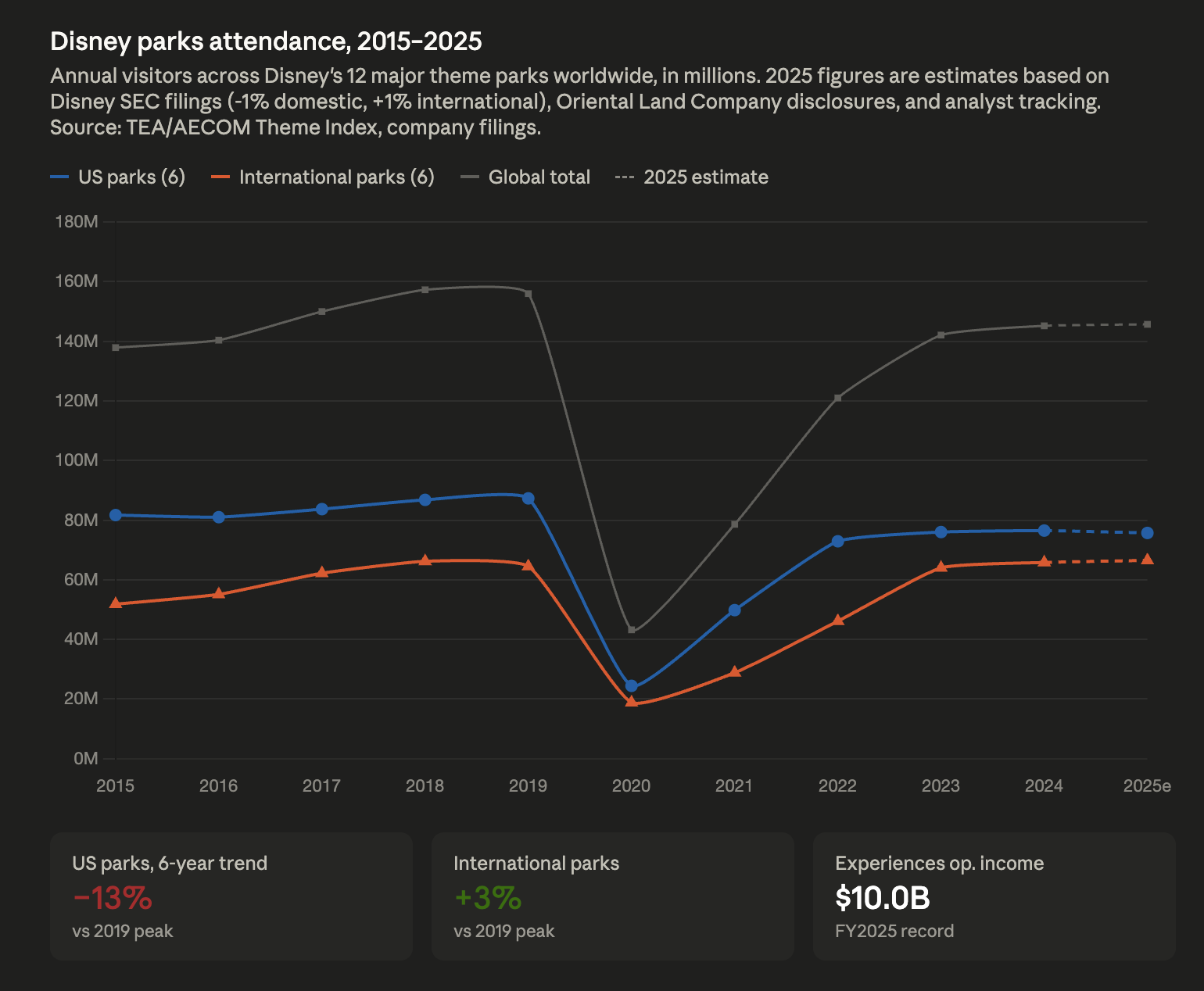

Disney is committing $60 billion to park expansions over the next decade. It’s building a brand-new resort in Abu Dhabi, and it’s nearly doubling its cruise fleet to 13 ships by 2031. There’s a new Avatar Land coming to Anaheim. Last quarter, the Experiences division crossed $10 billion in revenue for the first time.

But here’s a detail that isn’t getting enough attention: U.S. parks attendance was essentially flat in the most recent quarter outside of hurricane comparisons from the prior year. Disney isn’t growing by bringing more people through the gates. It’s growing by extracting more revenue per visitor through dynamic pricing that can push a single-day park pass to $199, through paid Lightning Lane line-cutting, through premium dining and merchandise, and through every incremental dollar it can squeeze from the guests who are already there. Disney has gotten away with quietly and “dynamically” raising the price at Disneyland and Disney World.

But that strategy has a ceiling, and Disney seems to be approaching it. Q2 guidance suggests attendance will be down, driven by international tourism headwinds, a Canadian boycott of American travel, the chilling effects of tariffs and trade tensions on global tourism, and a relatively strong dollar that makes U.S. vacations more expensive for foreign visitors. Disney said they’d “make it up in the back half of the year,” a phrase that tends to make investors nervous for good reason.

The macro picture is more concerning. The disruption to traditional employment from AI and automation, combined with persistent inflationary pressure on housing, healthcare, and education, is compressing discretionary spending for the American middle class, and broadly for the rest of the world. The American middle class is exactly the demographic that fills Disney parks and books Disney cruises. A Disney World vacation for a family of four now routinely costs within the ballpark of $5,000-$8,000. These are luxury price points, and the total addressable market for luxury experiences can contract sharply in a downturn. Add to this that NBCUniversal’s Epic Universe, a major new competitor park, opened this year, adding real competitive pressure to the business at precisely the wrong time.

Disney’s streaming business faces a parallel vulnerability. Much of its recent profitability, like its parks business, has come from price increases, a strategy that works until an economic downturn sends subscribers to the cancel button.

If Disney’s future is experiences, and experiences require consumers with significant amounts of disposable income, the company is building a castle on a foundation that macroeconomic forces are actively eroding.

Problem #3: Content Itself Is Being Commoditized

The media business is rapidly being commoditized, not slowly and not hypothetically, but right now. AI-powered video generation, image creation, music composition, and narrative tools are advancing at a pace that will, within the next several years, dramatically lower the cost and barrier to creating high-quality content.

The moat that Disney has enjoyed for a century (the ability to marshal enormous budgets, infrastructure, world-class talent, and cutting-edge proprietary technology to tell stories at a quality level that no one else could match) is sliding away. We are almost in a world where anyone with a laptop and a subscription to an AI creative suite can produce content that looks and sounds like it cost millions to make. The premium that audiences place on professionally produced content versus alternatives will compress rapidly.

IP obviously still matters. It is protected by law. You can’t generate Mickey Mouse or Star Wars without Disney’s permission. But the cultural gravity of any single IP weakens when the total volume of compelling content in the world explodes. Attention is finite. When everyone can tell stories, and there is no longer a barrier to creating high-quality visuals, the value of any individual storyteller, even a juggernaut like Disney, will decline.

This doesn’t mean Disney’s content business goes to zero. But it means that anchoring the entire company’s identity to content creation is the recipe for a losing long-term strategy. Disney needs to derive its value from things that can’t be commoditized by a model running on someone’s laptop.

What Can’t Be Commoditized

So: Disney’s content funnel is narrowing into a chokepoint with no clear new-IP engine. Its experiences business is extracting more from a stagnating visitor base while betting $60 billion on a consumer spending environment that’s deteriorating. And the underlying value of content production itself is being eroded by AI.

These are real and, in some ways, structural problems. But my opinion is that Disney already possesses the resources to build something far more durable than what it is today. The assets are already inside the building. They’re just not yet being deployed for the right purpose.

Disney Is Already a Robotics Company

This is not hyperbole. What Walt Disney Imagineering (their applied engineering division) has quietly built over the past several years is one of the most advanced entertainment robotics operations in the world, and increasingly, one of the most advanced robotics operations in any industry.

Disney, NVIDIA, and Google DeepMind are co-developing an open-source physics engine called Newton. Disney’s contribution is an internal simulator called Kamino (yes, that is named after what you think it is named after), which uses deep reinforcement learning to train robots, compressing what used to take years of development into days and weeks. Their BDX droids, the Star Wars-inspired robots now roaming parks worldwide, use spatial AI with onboard cameras to autonomously navigate complex environments, understand guest positions, and make real-time behavioral decisions. This project went from concept to deployment in under a year.

Disney’s robotics division has also built a self-balancing Olaf robot that taught itself bipedal locomotion through reinforcement learning. Aquatic robots in dolphin and manta ray forms operate autonomously using self-driving-car-grade sensor suites, and Stuntronics perform aerial acrobatics. Autonomous characters use computer vision and AI to independently interact with their environment, making their own decisions about where to go, what to do, and how to engage with humans.

Every single one of these capabilities is currently locked inside the theme parks. Every robot exists to entertain guests for a few minutes during a park visit. The technology they have developed at Disney is extraordinary. Its deployment, however, is absurdly constrained to just the parks.

Disney Has a Brand Trust Moat That No Technology Company Can Replicate

Consumer home robotics has been a graveyard. Jibo failed. Kuri failed. Amazon Astro struggled. Sony’s Aibo remains extremely niche outside Japan. The fundamental problem has been product-market fit: no company has convincingly answered the question, why would I want a robot inside my home?

Disney has an answer that no other company on Earth can give, because it’s not selling a robot. It’s selling a character.

A Disney home robot isn’t a utility device that reads you the weather. It’s a BB-8 rolling around your living room. It’s a Wall-E cleaning up your living room, or it’s Lightning McQueen beeping at your kids. It’s a companion that interacts with your family, tells stories, plays games, and creates emotional connections, built on the same reinforcement learning, spatial AI, and character animation technology that Imagineering has already proven works at scale in the parks.

Disney’s moat over other companies is brand trust. Despite the political turbulence the brand has faced over the past few years, Disney remains one of the most trusted brands worldwide for children and families. Parents trust Disney content to be in their homes. Extending that trust to Disney devices, AI-powered companions that are safe, age-appropriate, and wrapped in beloved characters, is a shorter leap than one might think.

This is the opposite of the Big Tech approach to home AI, where the value proposition is utilitarian, where it is simply about the benefits and what the product can do for you, and the brand identity is with a corporation that monetizes your data.

Disney’s brand permission is emotional connection, storytelling, and child safety. In a world where parents are increasingly anxious about their children’s relationship with technology, a Disney-branded AI companion that you trust to be in the room with your kids is a genuinely differentiated product, and one that no amount of VC funding or engineering talent at a robotics startup can replicate, because the trust took nearly a century to build.

Disney Has A Playground Like No Other Company In The World

The biggest issue most consumer robotics companies face is that consumers end up becoming the guinea pigs. Products are shipped and then heavily iterated on after launch, because no amount of simulation can fully predict the problems they will face in the real world. As a result, consumers feel cheated or disappointed when a product doesn’t live up to the hype or the promise out of the box, needs extensive software updates, or even has to be returned because certain components fail or don’t hold up in the field. Disney has something none of these companies have: fully functioning cities with foot traffic greater than that of many cities worldwide. Every person who enters a Disney property is, in some sense, consenting — and may even be a willing lab rat — for testing these robots. As a result, Disney could soft-test the tech and engineering, rapidly iterate in a SpaceX-style manner with its robots in its parks, and advance the program at a pace and cadence no other company on earth can match. Because it’s their park and their land, anyone who enters is waiving liability, which gives them tremendous leeway to test and advance these robots in real-world environments and make them extremely durable and reliable.

Disney Has Already Made Its Most Forward-Looking Bet, in Gaming

D’Amaro pushed Iger to invest $1.5 billion in Epic Games, giving Disney a digital presence inside Epic’s Fortnite ecosystem. When D’Amaro and Disney’s gaming chief Sean Shoptaw showed Iger the screen-time data (that Gen Z and Gen Alpha spend as much time on video games as on TV and movies combined), Iger called it “stunning” and wrote the check.

When D’Amaro pitched his CEO vision to the board, he specifically outlined a larger role for video games and the integration of gaming technology throughout Disney’s creative processes. There’s an expectation, articulated by Greenfield on Belloni’s podcast and echoed by others, that D’Amaro will need a career-defining strategic move in his first year, something analogous to Iger’s acquisition of Pixar. The most likely arena is gaming. Should Disney acquire Epic Games? Roblox? Build its own platform?

But the gaming opportunity is about more than a single acquisition. It’s about solving two problems simultaneously.

First, digital experiences diversify the single-points-of-failure risk in the content pipeline. If Disney can create and extend franchises through persistent digital worlds, and not just through theatrical releases, it multiplies the surfaces where IP can be born, tested, and scaled. A character that catches fire in a Fortnite collaboration or a Disney-branded digital world doesn’t need a $200 million movie to prove its value. Gaming becomes a franchise incubator alongside film, not subordinate to it. This directly addresses the new-IP problem: gaming is where younger audiences are discovering characters and stories, and Disney needs to be in that space not just as a licensor but as a creator.

Second, digital experiences are accessible at price points that physical experiences aren’t. You don’t need $8,000 for a family vacation to interact with Disney IP in a digital world. This directly addresses the consumer spending problem: it gives Disney a way to maintain its relationship with middle-class families even as premium physical experiences become less accessible.

And there’s a third dimension that’s being overlooked. Belloni pointed out that Disney+ is missing basic features to implement, such as in-app shopping, park day planning, games, social features, and community features for Disney fans. Disney+ today is just a streaming app. It should be the hub, or the tip of the spear, for the entire Disney ecosystem. It should be the digital front door that connects content, commerce, experiences, and community in a single platform. D’Amaro, who understands the operational side of the consumer relationship better than anyone at the company, is actually well-positioned to push Disney+ in this direction. The question is whether he has the product vision to get it done.

A Four-Pronged Disney

What I’m describing is not what Disney is planning. It’s what Disney could be if D’Amaro is willing to look at the assets he already controls and reimagine their purpose.

The opportunity is to reorganize Disney’s identity around four interconnected pillars:

The Media Flywheel

Content doesn’t go away; it becomes the engine that generates IP, characters, and narratives that feed every other pillar. Films, streaming shows, and animation continue, but their primary strategic value shifts from direct monetization to creating the thematic layer that makes everything else feel like Disney. Dana Walden’s expanded role as chief content officer, now overseeing film in addition to TV and streaming, already reflects the company’s continued commitment to content.

However, the content arm needs to remain sufficiently diversified to avoid single points of failure, and it desperately needs to address the new-IP creation gap. More shots on goal, not fewer. Success for the company in this vertical will need to be measured not just by box office or streaming numbers, but by the tentpole franchises, characters, and ecosystems it spawns.

AI and Robotics

The Imagineering capabilities, combined with the NVIDIA and DeepMind partnerships, form the basis of a genuine technology division. In the near term, this continues enhancing park experiences with more autonomous, emotionally engaging characters. In the medium term, it should become a consumer products play: home robots, AI companions, and interactive toys built on the same reinforcement learning and spatial AI that powers the park robots. In the long term, it positions Disney as one of the few consumer-trusted AI brands worldwide. This is the pillar that addresses content commoditization head-on: you can generate a video that looks like a Marvel movie with AI, but you cannot generate a walking, emotionally intelligent Disney robot in your living room.

Digital Experiences

D’Amaro should double down on the Epic Games investment and create deeper Fortnite and video game integrations. Disney should also, separately or in collaboration with Epic, build its own persistent digital world where its IP lives and where younger demographics can engage with the brand on their own terms. Gaming becomes a fantastic location for franchise creation and a testing engine alongside film, solving much of the uphill battle when it comes to creating, promoting, and launching new IP.

Disney+ evolves from a streaming app into the digital front door for the entire Disney ecosystem. Content, commerce, parks, gaming, and community all come together on a super app.

Physical Experiences

Parks, cruises, resorts, and live events remain the highest-margin pillar. The $60 billion expansion continues. But physical experiences are enhanced by robotics and AI: more autonomous characters, more immersive environments, and more personalized interactions, creating an experience gap that competitors, including Universal’s Epic Universe, can’t easily close. This is the pillar that benefits from the other pillars working. Better content creates better IP, better robotics creates better attractions, and digital experiences create greater demand for physical ones.

The Chapek Problem

There is an obvious counterargument to everything I’ve written, and his name is Bob Chapek.

Chapek was also a parks guy. He also rose through the Experiences division. He also tried to impose a new strategic vision on Disney when he became CEO. The company rejected it. His reorganization, which created a centralized distribution arm under Kareem Daniel, was widely criticized, alienated Hollywood’s creative community, and contributed to a tenure so disastrous that Disney had to pull Iger out of retirement to fix it.

If the last parks-focused CEO couldn’t change Disney’s culture, why would this one?

There are some meaningful differences between how the two succession plans moved. Chapek’s failure wasn’t primarily about strategy; it was about execution, temperament, and the impossible dynamics of following a living legend who didn’t actually want to leave. Iger played a lot of politics and undermined Chapek behind the scenes. The decision to have Iger depart in March rather than lingering through year-end is a deliberate attempt to avoid that shadow. James Gorman, now board chair, explicitly addressed this stating in no uncertain terms “We won’t have the drama we had last time.”

D’Amaro also has something Chapek didn’t: the benefit of hindsight, a content-side partner in Dana Walden who is no longer competing with him, has free rein to operate in her part of the business, and a board that has spent three years trying to learn from its mistakes. Whether that’s enough to overcome Disney’s well-documented institutional resistance to change remains to be seen.

The issue however for D’Amaro is that the problems I’ve described won’t wait for Disney to get comfortable. Content commoditization is happening now. Consumer spending pressure is building now. The park attendance plateau is very visible now. The window for bold strategic repositioning doesn’t stay open indefinitely, and the companies that move first, that redefine themselves before market forces do, are the ones that survive transformational moments in their industries.

A question I’ve kept asking myself, given recent developments in the industry, is whether Disney is the next big acquisition target after Warner Brothers. It is very possible that Disney could be next. Now, granted, Disney is substantially bigger than Warner Brothers, and so it’s going to take much deeper pockets and a much more well-capitalized buyer for Disney to be acquired. But if structural pressures continue to accumulate at the current rate, Disney could shrink, which might finally make it a likely acquisition target.

There are companies that would be pretty solid fits to acquire Disney. In my opinion, the biggest one is Apple. Apple and Disney’s partnership, which has lasted for decades, began when Steve Jobs sold Pixar to Disney. It has persisted in some form or another since. There are clear synergies between the brands, and the companies share a largely safe and clean image.

One of the many things I had read and heard from analysts and commentators when Iger returned to Disney was that Iger would be the last CEO of Disney. What they meant was that Iger was back mainly to facilitate a sale of the company. Apple was always considered to be the main suitor in this conversation. That proved in the end not to be true, but just because it wasn’t true then doesn’t mean it could not be true later.

If D’Amaro is unable to reposition Disney for the modern era, there is a realistic chance that Disney is sold. It could end up at a company that has a long history of collaborating with the company, like Apple, or it could end up with another player, a dark horse, not the Ellisons but perhaps someone like them, who has deep pockets and is interested in buying a legacy business with immense prestige that they believe they could turn around.

The Question for D’Amaro

None of this is what Josh D’Amaro was hired to do. He was hired because he runs the division that makes the most money, and the board wanted continuity and operational excellence. The safe play is to keep doing what’s working: expand the parks, grow the cruise line, lean on tentpole films to feed the experience machine, maybe make a splashy gaming acquisition, and let Disney’s brand carry the rest.

But the problems I’ve outlined (content concentration risk with no new-IP engine, consumer spending headwinds against a stagnating visitor base, and the commoditization of media itself) are not problems that operational excellence alone can resolve. They’re very structural. And they require Disney to become something different from what it is today.

It is perhaps by sheer coincidence, or not, that D’Amaro has been sitting on the exact assets that could make that transformation possible. The robotics. The AI partnerships. The gaming beachhead. The experience design expertise. It’s all there, inside the exact division he’s run for five years.

Everyone expects D’Amaro’s career-defining move to be an acquisition, an Epic Games or Roblox-scale deal that signals ambition and gives Wall Street a narrative. That might happen, and it might even be the right call. But the truly career-defining move would be something much bigger: recognizing that Disney’s future isn’t about being a better version of what it already is. It’s perhaps about reinventing it to become something it hasn’t been before.

The pieces are all there. The question is, will D’Amaro be the guy who’ll be able to put it all together?